Blog

How Credit Card and Personal Loan Settlement Works Under Indian Law

Financial obligations can become stressful if your repayments exceed the capacity of your account. In these instances it is important to understand the debt settlement process in India is essential for those who aren’t able to pay their loans on time. Personal loans and credit card settlement are legal ways to settle outstanding dues by negotiations with lenders.

We are Trust Law Associates. We assist people to comprehend the legal framework that governs the settlement of debt in India and assist them in navigating secure and legal solutions.

What is Debt Settlement in India?

A debt settlement agreement in India is an agreement that is legally binding between a borrower as well as a lender in which the borrower pays the lender a smaller amount in order to close the account. This is usually the case when the borrower is in serious financial problems and is not able to pay the entire amount.

In the majority of cases, debt settlement in India is utilized to resolve debts in cases where the repayment is not possible. It is a way to avoid lengthy defaults as well as legal escalation however, it should be managed with care and a clear legal framework.

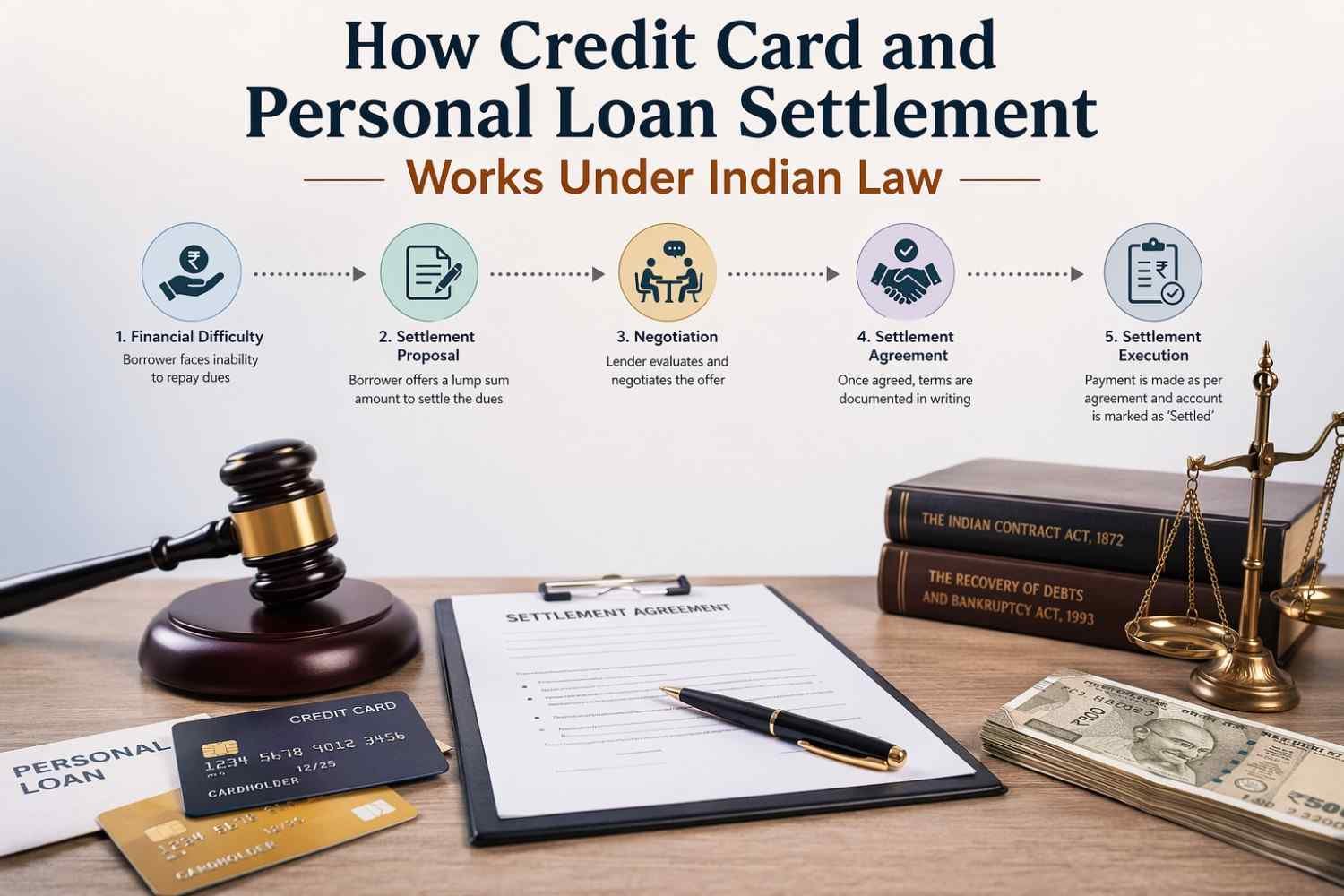

Understanding the Loan Settlement Process

The procedure of loan settlement involves a formal discussion between the borrower as well as the financial institution or bank.

Key Steps:

- The financial assessment of the borrower

- Negotiation of reduced repayment amounts

- Agreement between both parties

- Payment of the final settlement and closing

In this procedure of settling loans it is crucial to ensure that all conditions are documented clearly in order to avoid disputes later on. Many borrowers prefer credit settlements in India by contacting legal professionals to ensure that they are transparent.

Credit Card Debt Relief Options

Credit cards are often accompanied by very high rates of interest, making the repayment process difficult for a lot of people. Debt relief for credit cards by settlement is an effective solution for those facing overdue payment issues.

When you opt to go through the debt-settling option in India the credit card charges are reduced to a reasonable amount. However, the borrowers must be aware that even though relief is offered, it can affect credit scores.

RBI Guidelines for Loan Settlement

The RBI guidelines for loan settlement govern the way banks and financial institutions deal with cases of default and recovery. These guidelines guarantee an equitable treatment of borrowers and fair settlement procedures.

In accordance with RBI Guidelines for the settlement of loans:

- Banks are required to follow reasonable recovery practices

- The borrower must be provided with the appropriate settlement options

- Documentation should be clear and legally compliant

These guidelines play a crucial function in ensuring the settlement of debt is conducted in India is done ethically and legally.

Legal Notice for Loan Default

If a borrower does not pay back the loan, banks usually issue a legal notice of default on loans. The notice is a formal notice requiring the repayment within a certain date.

Receiving notice of a legal notice of default on loans is not a requirement for immediate legal action. However, not addressing it could lead to grave consequences. Many borrowers decide to opt to settle their debts in India during this time to avoid court action.

It is advisable to take action to these notices in accordance with the proper guidance of the law.

Legal Framework of Debt Settlement in India

According to Indian legislation, debt settlement in India is acknowledged as a valid means to resolve financial disputes between lenders and borrowers. However it has to be done correctly to protect legal rights.

Important legal considerations include:

- Written settlement agreement

- A clear repayment agreement

- Proper closure documentation

- Legal confirmation of settlements on accounts

In the absence of proper documentation or documentation, even a bank account that is settled can lead to problems in the future.

Risks Involved in Debt Settlement

While the debt settlement process in India can provide relief, it is not without risk:

- Credit score can be negatively affected by negative credit

- The difficulty in getting future loans

- Potentially report to be “settled” instead of “closed”

Despite these risks the option of debt settlement in India is still a viable alternative for those who are in financial hardship.

How Trust Law Associates Can Help

Trust Law Associates Trust Law Associates we are experts in helping clients navigate the process of settling debts in India with full legal assistance.

The services we offer include

- Legal advice for the resolution of loan disputes

- Assistance in negotiating with banks

- Processing of the process of loan settlement Documentation

- Respond in response to legal notice regarding default on loan

- End-to-end settlement assistance

We guarantee that every debt settlement in India matters is done professionally and legally.

Conclusion

Knowing about how to settle debt in India is essential for those struggling with debt repayment. It doesn’t matter if it’s due to credit card charges as well as personal loans, the process of settlement can be structured to handle the financial burden. From the procedure of loan settlement to the process of dealing with a legal notice of default on loans each step demands care and attention to the law. With guidance from a professional such as Trust Law Associates and Trust Law Associates, borrowers can solve their financial concerns in a safe manner and achieve financial stability.